Loading subject page…

- Accounting

- Asset Management

- Understanding Asset Capitalization

Micro-course: Asset Management

2,138 views

Learn key concepts and earn your certificate.

Understanding Asset Capitalization

00:00

01:25

Video Summary: Asset Capitalization Explained

Asset capitalization basics trip up even experienced managers when capital budgets are under scrutiny and every purchase decision carries financial weight. Understanding asset capitalization — recording a long-term purchase on the balance sheet rather than expensing it immediately — directly shapes how your team's spending decisions appear in financial reports. Get this wrong and you misrepresent costs, distort profitability, and lose credibility with finance. Watch the full video on JoVE Coach to master this concept with expert-led visuals and step-by-step explanations.

- Recognize which team purchases qualify as capitalized assets versus immediate operational expenses, applying the core criteria of ownership, operational use, and multi-year useful life

- Structure capital expenditure requests with confidence by understanding how long-term assets are recorded, depreciated, and tracked across accounting periods

- Align procurement decisions with your organization's capitalization thresholds and fixed asset policies to avoid misclassification and financial restatements

- Manage depreciation timelines for your department's assets using straight-line and other depreciation methods to accurately forecast budget impact year over year

- Lead cross-functional conversations with finance and accounting teams using precise asset capitalization language, improving your credibility in budget reviews

- Set internal controls and documentation standards for your team's asset registry, ensuring physical and intangible assets are properly recorded throughout their lifecycle

- Navigate ROI conversations on major equipment or infrastructure investments by connecting asset capitalization principles to asset turnover and long-term value generation

- Build a financially literate team culture where managers and senior individual contributors understand how capital spending decisions affect the organization's balance sheet

Asset Capitalization Explained

Picture this: your team just approved a significant equipment purchase — new machinery, a software platform, or specialized infrastructure. The invoice lands on your desk. Does this go straight to the expense line and reduce this quarter's operating budget? Or does it sit on the balance sheet as a long-term asset? If you hesitate before answering, you're not alone. Misclassifying capital expenditures is one of the most common and costly financial errors managers make — and it rarely comes from dishonesty. It comes from not understanding asset capitalization basics at the point of decision.

Why Most Managers Struggle With This

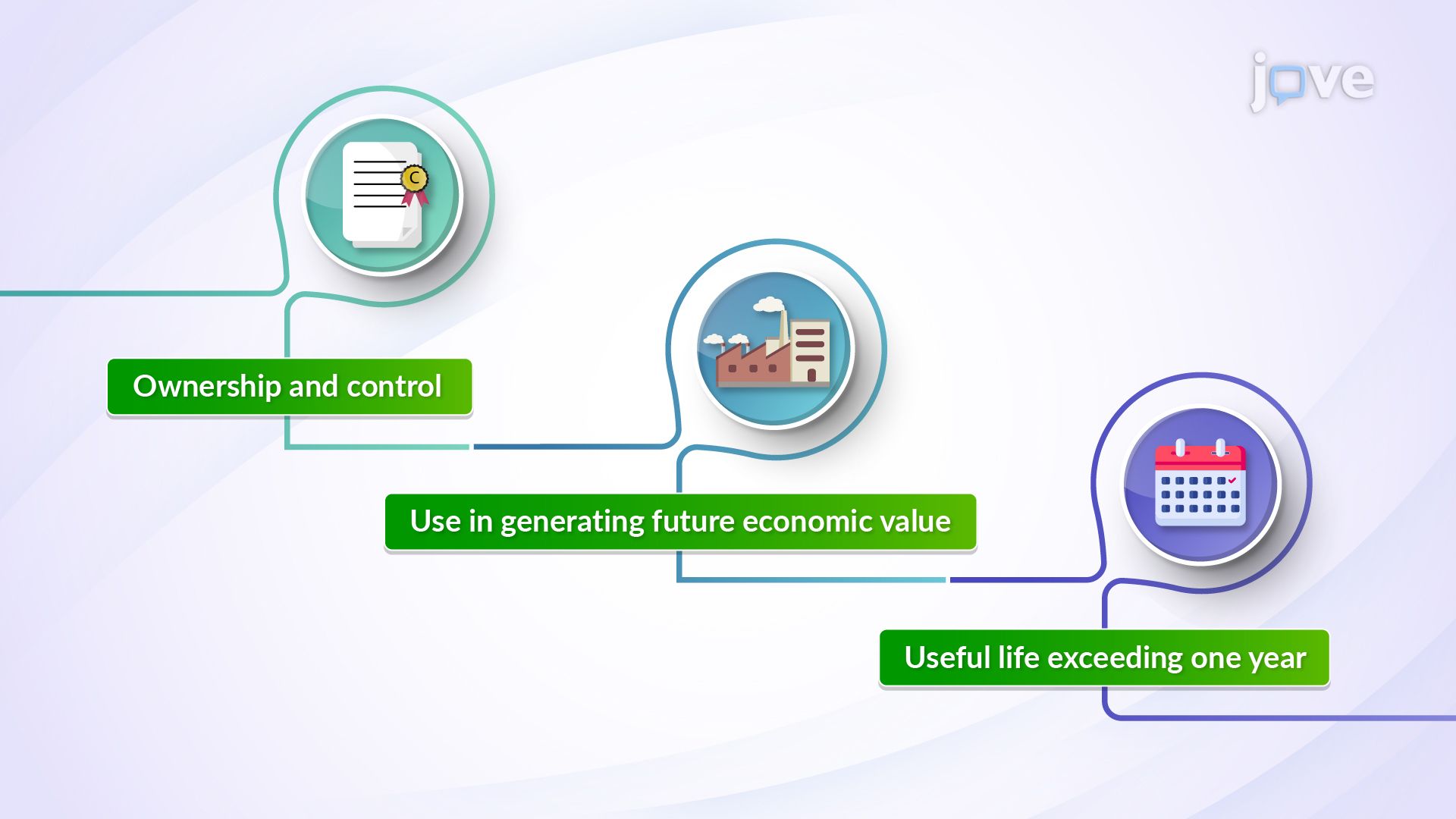

The root problem is that most managers are trained in their functional discipline — operations, engineering, marketing, or sales — not in financial accounting. When a purchase arrives, the instinct is to treat it like any other cost: spend it, record it, move on. But asset capitalization follows a different logic. A cost is only capitalized when the item is owned and controlled by the business, actively used in operations to generate future economic value, and has a useful life extending beyond one accounting year. Miss any one of these three criteria and you've made a classification error that your finance team will eventually catch — and your leadership credibility will take the hit.

A Framework That Works: The Three-Gate Test

Before any significant purchase reaches the approval stage, run it through what practitioners call a Three-Gate Test:

Gate 1 — Ownership and Control: Does the business own this asset outright, or is it leased, rented, or licensed? Owned assets that meet other criteria are capitalized. Operating leases and short-term rentals are expensed.

Gate 2 — Operational Value: Will this asset directly support revenue generation or core operations over time? A piece of manufacturing equipment qualifies. A one-time consulting engagement does not.

Gate 3 — Useful Life Beyond One Year: Does the asset's productive life extend past the current accounting period? If yes, capitalization applies. If it's consumed within twelve months, it's an expense.

Once an asset clears all three gates, it moves onto the balance sheet as a non-current fixed asset. From that point, depreciation — most commonly using the straight-line method — spreads the cost across the asset's useful life, creating annual expense recognition rather than a single-period hit. This protects quarterly profitability and gives a more accurate picture of operational performance. For teams managing physical infrastructure, this directly affects asset lifecycle planning and maintenance scheduling decisions.

How to Apply This in Your Next Budget Review

In practice, asset capitalization becomes a leadership skill during budget planning and capital expenditure conversations. When presenting a major purchase to finance or senior leadership, come prepared with the asset's estimated useful life, projected depreciation schedule, and its anticipated ROI — specifically, how it contributes to the asset turnover ratio over time. The asset turnover ratio (Net Revenue ÷ Average Total Assets) is a metric senior stakeholders use to assess whether capital investments are generating proportional returns. Managers who can articulate this connection signal financial maturity that accelerates career progression.

Internally, establish a clear capitalization policy for your team. Define your organization's capitalization threshold — typically a minimum dollar value below which items are expensed regardless — and document it in your asset registry. This creates consistency, reduces audit risk, and ensures your team's asset lifecycle data remains accurate for long-term planning.

Common Mistakes to Avoid

The two most damaging errors are over-expensing (writing off capitalizable assets immediately to inflate short-term cost control metrics) and over-capitalizing (pushing routine maintenance or consumable costs onto the balance sheet to avoid hitting expense budgets). Both distort financial statements and can trigger compliance reviews. Establish a peer-review checkpoint within your team before submitting any capital expenditure request above your organization's threshold. A second set of eyes at this stage catches misclassification early — before it becomes an audit finding.

Frequently Asked Questions

It means recording a significant purchase as a long-term asset on the balance sheet rather than a one-time expense. Instead of the full cost hitting your budget immediately, it's spread over the asset's useful life through annual depreciation. For managers, this directly affects how capital spending decisions show up in financial reports and how your team's budget performance is measured. ---

When a purchase is capitalized, it doesn't reduce your operating budget in the year of purchase — the cost is recognized gradually through depreciation. This means large equipment or infrastructure investments can be made without distorting your team's quarterly expense line, but the depreciation charge will appear in future periods. Understanding this helps you plan more accurately and set realistic budget expectations with your leadership team. ---

Any time a purchase is significant in value, has a useful life beyond one year, and will be actively used in operations, loop in finance before approval. Most organizations have a capitalization threshold — a minimum dollar amount — above which purchases must be assessed for balance sheet treatment. Engaging finance early prevents misclassification, avoids budget restatements, and positions you as a commercially aware leader. ---

Depreciation methods determine how an asset's cost is allocated across its useful life. Straight-line depreciation spreads the cost equally each year, making budget forecasting predictable and straightforward. Other methods, such as declining balance, front-load more cost in early years. The method your organization uses affects annual expense recognition, profitability reporting, and how asset value appears on the balance sheet — all of which matter when you're justifying future capital investments. ---

Yes — if the machinery has a useful life beyond one year and meets capitalization criteria, expensing it in full in a single quarter is a misclassification. This overstates expenses in that period and understates asset value on the balance sheet, distorting both profitability and financial position. Finance or an auditor will likely flag this, and it may require a restatement. The right approach is to capitalize the asset and depreciate it over its useful life. ---

Not at all — and this is exactly why concepts like asset capitalization basics are worth investing time in as a leader. You don't need to build depreciation schedules from scratch; your finance team handles the technical accounting. What matters is that you understand the criteria, ask the right questions before approving capital purchases, and can hold an informed conversation with finance during budget reviews. That competency alone sets you apart from most people managers. ---

Leaders who understand how capital spending decisions appear on financial statements make better resource allocation choices, earn more credibility with senior stakeholders, and are trusted with larger budgets. When you can connect a team investment to long-term asset value, depreciation impact, and ROI — rather than just the upfront cost — you signal strategic financial thinking. This is the kind of commercial acumen that accelerates progression from functional manager to senior leadership. ---

A strong next step is understanding how to calculate and interpret the asset turnover ratio — a key performance indicator that measures how effectively your organization uses its asset base to generate revenue. Paired with asset capitalization knowledge, this gives you a complete picture of both how assets are recorded and how their performance is measured, which makes you significantly more effective in capital planning conversations and long-term investment decisions.

Understanding Internal Control explores a complementary area of Accounting, while Understanding Asset Capitalization focuses on the specific concept covered in this video. Understanding both helps you build a stronger foundation in Accounting.

A basic understanding of Cost Basis vs. Fair Value Accounting is helpful before diving into Understanding Asset Capitalization. If you are starting from scratch, the Asset Management series builds knowledge progressively, so beginning from the first video requires no prior background in Accounting.

The ideas in Understanding Asset Capitalization show up in everyday Accounting contexts, often alongside concepts like Introduction to Accounting. This video connects the theory to practical situations you may encounter in coursework or exams.

After Understanding Asset Capitalization, the natural next step is Asset Disposal: Sales, Trade-Ins and Write-Offs in the Asset Management series. Following the playlist in order helps concepts build on each other without gaps.

The Understanding Asset Capitalization video runs for 1 minute, so you can cover the core concept in a single focused study session without needing a long block of time.

Related Micro-courses

9 Concepts

23 Concepts

21 Concepts