Loading subject page…

- Accounting

- Preparation of Income Statement

- Single-Step vs. Multi-Step Income Statement

Micro-course: Preparation of Income Statement

5,683 views

Learn key concepts and earn your certificate.

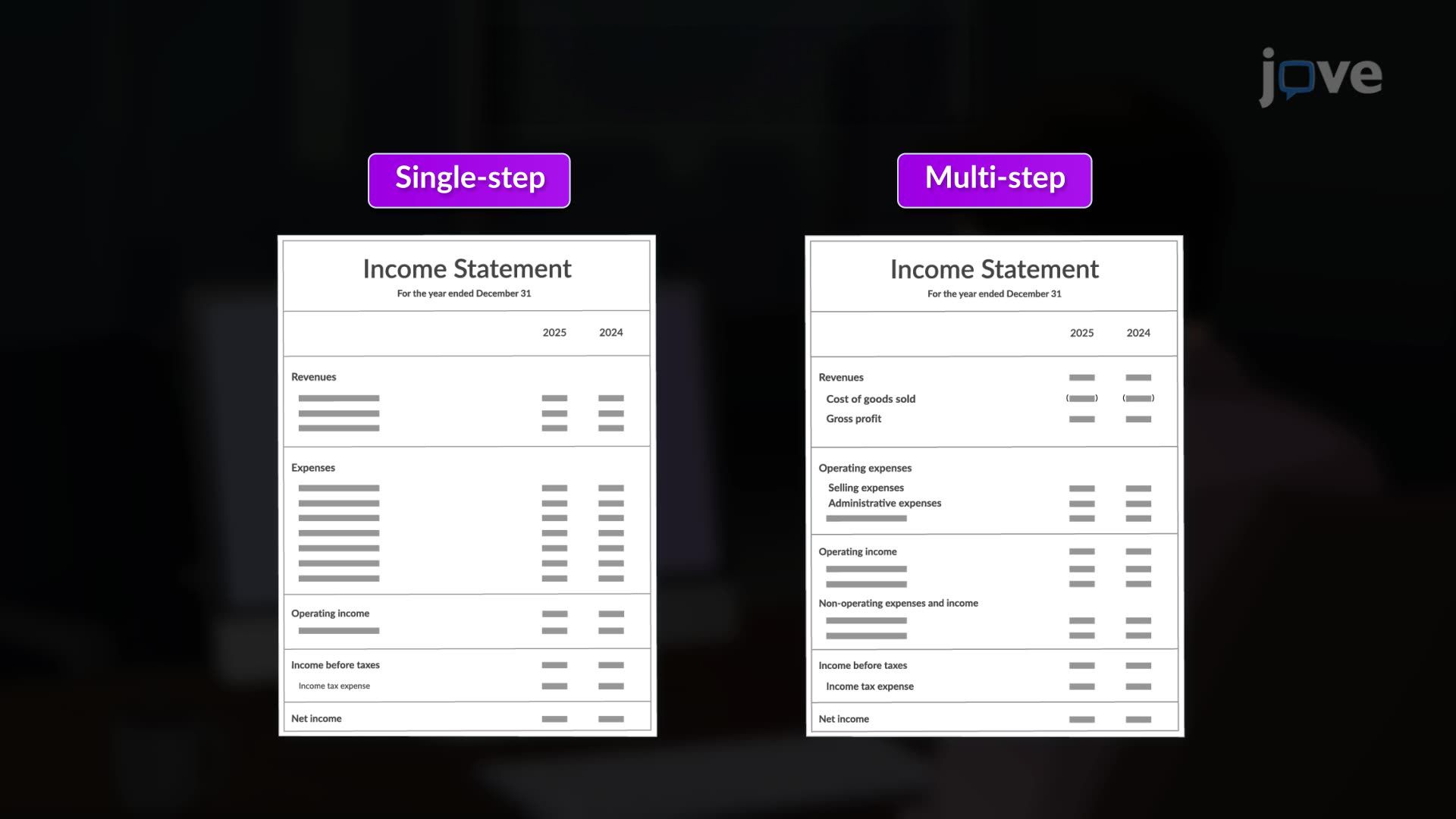

Single-Step vs. Multi-Step Income Statement

00:00

01:24

- Recognize which income statement format your organization uses and understand what financial story it is designed to tell

- Interpret revenue and expense line items accurately so you can contribute meaningfully to budget discussions and financial planning conversations

- Distinguish between operating and non-operating income sources to assess where your team's work directly drives business performance

- Manage cost visibility by understanding how Cost of Goods Sold (COGS) and gross margin are tracked — or hidden — depending on the format used

- Align your team's resource requests with the financial structure your organization reports against, making your business cases more credible

- Navigate cross-functional conversations with finance and senior leadership using the right terminology — net income, net margin, EBITDA — without misrepresenting the numbers

- Structure operational decisions with a clearer view of how revenue recognition and layered expenses affect overall profitability in your business unit

- Lead more effective performance reviews and planning cycles by connecting your team's output to the financial metrics that matter at the leadership level

Single-Step vs. Multi-Step Income Statement Explained

Picture this: you're sitting in a quarterly business review and your finance partner pulls up the income statement. Leadership is discussing whether to approve headcount for your team. You nod along, but you're not entirely sure whether the numbers being debated reflect gross profit or net income — or why that difference matters for your request. This is exactly the kind of moment where understanding the single-step vs. multi-step income statement stops being a finance topic and becomes a leadership competency.

Why Managers Struggle to Read Income Statements Confidently

Most managers in non-finance roles were never formally taught to distinguish between income statement formats. They know revenue is good and expenses are bad — but the structure beneath that is often opaque. The result is that many managers either defer entirely to finance or misread what the numbers are actually saying.

The core issue is that the two formats answer different questions. A single-step income statement totals all revenues, subtracts all expenses, and arrives at net income — clean, fast, and easy to read. But it doesn't show *where* profitability breaks down. A multi-step income statement separates operating from non-operating income, and breaks out selling, general, and administrative expenses from the Cost of Goods Sold (COGS). That layered structure reveals the *gross margin* — a critical number for any manager overseeing a team that produces, sells, or delivers a product or service.

If you manage in a business unit with a complex cost structure — multiple revenue streams, distinct selling and production costs — the single-step format may actually obscure the information you need to make sound operational decisions.

A Practical Framework: Match the Format to the Business Model

Think of income statement formats through the lens of a simple diagnostic:

- Simple, service-based, or small-scale operations → Single-step format works well. Revenue streams are limited, costs are straightforward, and net income tells the essential story.

- Complex, multi-layered, or product-based operations → Multi-step format is necessary. It surfaces gross margin, separates operating performance from one-time gains or losses, and lets leadership track EBITDA and net margin accurately.

As a manager, the practical takeaway is this: when your organization uses a multi-step format, pay close attention to gross margin (revenue minus COGS) *before* you look at net income. Gross margin tells you how efficiently your core operations are running. Net income reflects everything — including items outside your control, like interest income from asset sales or non-recurring expenses.

Apply the MECE principle (Mutually Exclusive, Collectively Exhaustive) here: treat each section of a multi-step statement as a distinct diagnostic zone. Operating performance is separate from non-operating performance. Selling costs are separate from administrative overhead. This prevents conflation — and prevents misguided decisions like cutting headcount to fix a margin problem that actually originated in procurement.

How to Apply This in Budget Conversations and Planning Cycles

In your next budget discussion or team planning cycle, use these three questions to anchor your financial fluency:

1. What does the gross margin tell us? If your team contributes to revenue or COGS, your operational decisions directly affect this number. 2. Are the numbers we're discussing operating figures or total net income? This distinction matters when evaluating team performance versus business-wide factors. 3. Which costs are fixed and which are variable in this statement? This is where resource planning decisions — including hiring, tools, and vendor spend — need to be grounded.

You don't need to be a finance expert to lead effectively. But you do need to be a fluent reader of the financial language your organization uses. Understanding whether your business reports on a single-step or multi-step basis is the foundation of that fluency.

Common Mistakes Managers Make When Interpreting Income Statements

Equating net income with operational health. Net income includes non-operating items that have nothing to do with your team's performance. A strong net income quarter can mask poor gross margin — and vice versa.

Assuming one format is superior. Neither format is universally better. The right format depends on complexity, industry norms, and what decisions the business needs to make. Pushing for more detail than the business model requires adds noise, not clarity.

Ignoring the profit and loss statement until year-end. Managers who engage with financial statements only during annual reviews miss early signals. Build a habit of reviewing the P&L monthly — even at a summary level — so trends become visible before they become problems.

Frequently Asked Questions

It determines how much financial detail you have access to when making operational decisions. A single-step format gives you a clean bottom line — useful for simple operations, but limited for diagnosing where profitability is being gained or lost. A multi-step format reveals gross margin, operating income, and non-operating items separately, giving you far more leverage in budget conversations, resource planning, and performance analysis. ---

Frame your request in the language of the financial structure your organization uses. If your business reports gross margin separately, show how your team's work protects or improves that number — not just total revenue. Decision-makers respond better to proposals that speak to the metrics they're already tracking. Understanding whether costs associated with your team appear above or below the gross profit line also helps you position your request accurately. ---

Every team appears somewhere in the income statement — either in COGS, selling expenses, or general and administrative costs. Knowing which category your team's costs fall into tells you how your budget is scrutinized. Administrative costs are often the first target in a margin-improvement push. If you understand that dynamic, you can proactively demonstrate the return on your team's spend rather than waiting to defend it under pressure. ---

Use the multi-step format's structure as a meeting agenda framework. Start with gross margin — what did we produce or deliver, and at what cost? Then move to operating expenses — what did we spend to sell, support, and administer? End with net income or contribution margin. This sequence keeps the team focused on controllable costs first and prevents conversations from jumping immediately to the bottom line without examining how you got there. ---

This is a classic gross margin versus net margin diagnostic. Revenue can rise while net margin falls if COGS grew faster than revenue — meaning you're selling more but keeping less per unit. Alternatively, non-operating costs or one-time charges may be dragging down net income. A multi-step income statement makes this visible immediately. If you only have a single-step statement, you'd need to request a breakdown of expenses by category to identify the source of the compression. ---

Not at all. If you can read a basic budget report and understand the difference between revenue and expenses, you have enough foundation to work with income statement formats. The goal isn't to replace your finance partner — it's to ask better questions, interpret reports with more confidence, and connect your team's work to the numbers leadership is watching. This is a skill that develops quickly with consistent practice. ---

Financial fluency is one of the clearest differentiators between managers who stay at their current level and those who advance into senior leadership. Leaders who can read, interpret, and speak to financial statements earn more credibility with finance partners, executives, and cross-functional stakeholders. It also sharpens your instincts during planning cycles — you make faster, more defensible decisions when you understand the financial structure your organization operates within. ---

The natural next step is understanding how to calculate and interpret gross margin percentage — (Gross Profit ÷ Revenue) × 100 — and how to use it as a diagnostic tool across reporting periods. From there, exploring EBITDA as a measure of operational performance and learning how revenue recognition policies affect when and how revenue appears on the statement will round out your financial leadership toolkit significantly.

Introduction of the Balance Sheet explores a complementary area of Accounting, while Single-Step vs. Multi-Step Income Statement focuses on the specific concept covered in this video. Understanding both helps you build a stronger foundation in Accounting.

A basic understanding of Net Profit is helpful before diving into Single-Step vs. Multi-Step Income Statement. If you are starting from scratch, the Preparation of Income Statement series builds knowledge progressively, so beginning from the first video requires no prior background in Accounting.

The ideas in Single-Step vs. Multi-Step Income Statement show up in everyday Accounting contexts, often alongside concepts like Introduction of the Cash Flow Statement. This video connects the theory to practical situations you may encounter in coursework or exams.

After Single-Step vs. Multi-Step Income Statement, the natural next step is Other Comprehensive Income in the Preparation of Income Statement series. Following the playlist in order helps concepts build on each other without gaps.

The Single-Step vs. Multi-Step Income Statement video runs for 1 minute, so you can cover the core concept in a single focused study session without needing a long block of time.

Related Micro-courses

20 Concepts

17 Concepts