Loading subject page…

- Accounting

- Preparation of Cash Flow Statement

- Understanding Financing Activities

Micro-course: Preparation of Cash Flow Statement

5,288 views

Learn key concepts and earn your certificate.

Understanding Financing Activities

00:00

01:24

- Distinguish financing activities from operating and investing activities to accurately read a cash flow statement and communicate financial context to your team

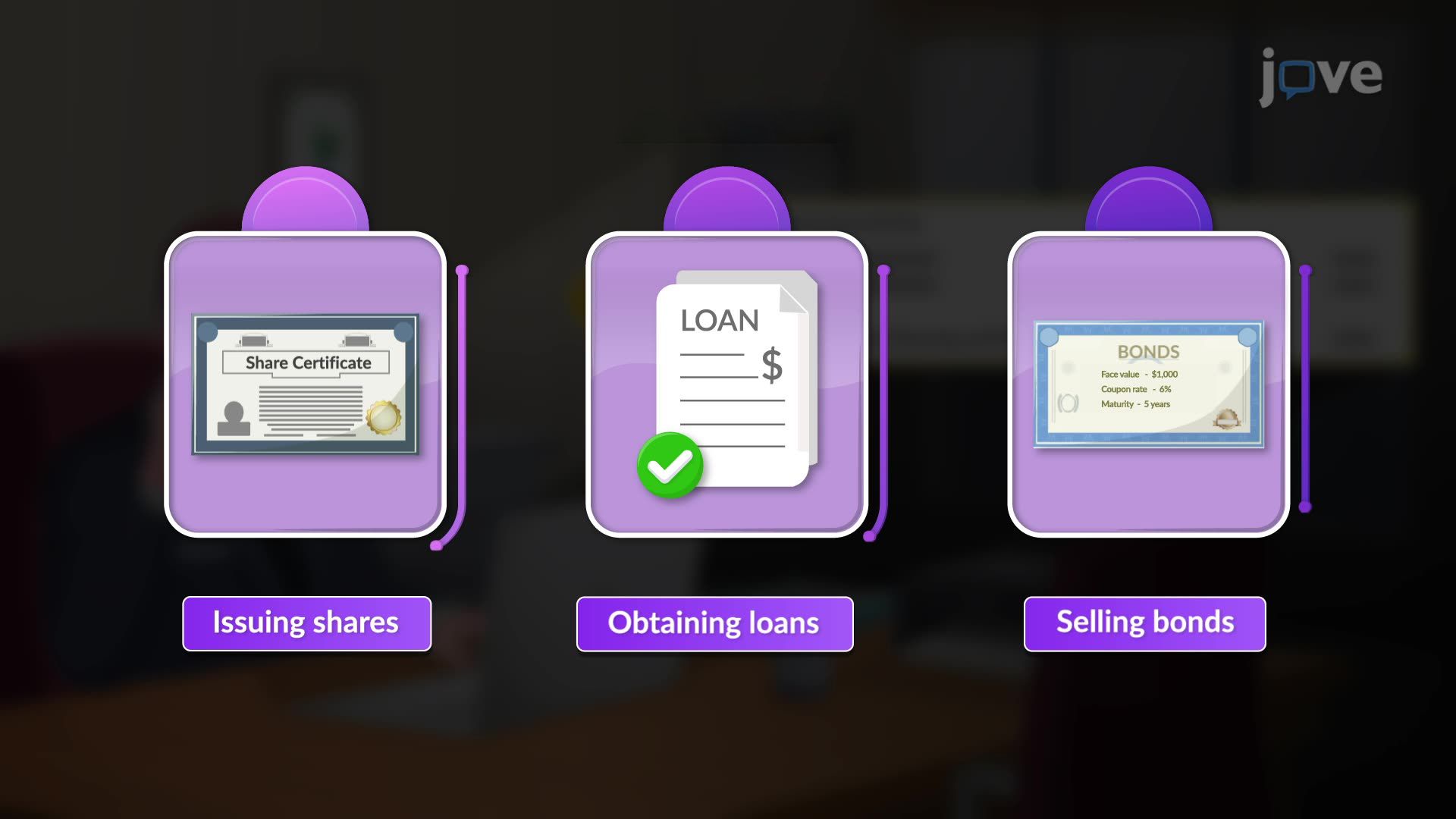

- Recognize cash inflows — such as equity issuances, bond sales, and loan proceeds — and explain their strategic implications to senior stakeholders

- Identify cash outflows — including debt repayments, dividend distributions, and share buybacks — to assess a company's near-term financial commitments

- Analyze the financing section of a cash flow statement to evaluate whether a business is funding growth through debt, equity, or internal reserves

- Align your team's resource planning conversations with the organization's broader financing strategy and capital structure decisions

- Navigate stakeholder conversations about financial sustainability by interpreting what the financing activities section reveals about long-term business direction

- Structure informed recommendations to leadership by connecting net cash flow trends in financing activities to operational capacity and team investment decisions

- Build financial fluency as a manager by understanding how non-cash expenses and working capital changes interact with overall cash flow reporting

Financing Activities Explained

Picture this: your organization has just announced a significant headcount expansion, and you're in a leadership meeting trying to understand how it's being funded. Someone references the cash flow statement. The room moves on quickly — but you're left wondering what the financing section actually tells you, and why it matters for decisions your team will feel directly. This is one of the most common gaps in managerial financial literacy, and it has real consequences.

Why Managers Struggle to Read Financing Activities

Most managers can follow a profit-and-loss statement intuitively — revenue comes in, costs go out. The cash flow statement feels less intuitive because it separates money movement into three distinct categories: operating activities (the day-to-day), investing activities (acquiring or offloading long-term assets), and financing activities (how the business funds itself structurally). The financing section is where the organization's capital strategy lives. Managers who skip it miss the full picture of financial health — and lose credibility in senior conversations.

The common mistake is treating financing activities as a finance team concern rather than a leadership context. In reality, understanding whether your company raised capital through new equity or took on long-term debt tells you something fundamental about expectations, pressure, and pace. If the business issued shares, investors expect growth. If it took on significant loans, there are repayment obligations that will shape future budget cycles.

A Framework for Reading the Financing Section

Think of financing activities through a simple three-lens framework:

1. Capital Raising Lens — Inflows from issuing shares or borrowing signal that the business is investing in future capability. As a manager, this is the context behind new headcount approvals, technology investments, or market expansion signals.

2. Obligation Lens — Outflows from loan repayments or bond redemptions tell you the organization has structured financial commitments. This affects how flexible the budget really is. When senior leadership seems conservative on discretionary spend, this section often explains why.

3. Shareholder Return Lens — Dividend payments and share repurchases signal what the business is prioritizing: returning value to existing investors rather than reinvesting in growth. For managers making a case for new resources, this context is essential.

This mirrors how financial analysts apply the DuPont Framework — breaking performance into component parts to understand the full picture rather than reacting to a single number.

How to Apply This in Leadership Conversations

You don't need to build the cash flow statement yourself. What you need is the ability to read the financing section and ask the right questions. Before your next budget conversation or strategic planning session, pull the most recent cash flow statement and look at three things: What was the net change in long-term debt? Were dividends paid? Was any new equity raised?

Use these as anchors. If the business repaid significant debt while also paying dividends, the organization is in a de-leveraging, steady-state posture — ambitious resource requests will need very clear ROI framing. If new equity was raised, the business is in growth mode — that's the right moment to advocate for your team's investments.

This is the managerial application of cash flow literacy: not accounting expertise, but contextual intelligence that makes you a sharper, more credible voice in the room.

Common Mistakes Managers Make

The most frequent mistake is conflating profitability with cash availability. A business can report strong net income and still face cash constraints — because profit is an accounting measure, while cash flow reflects actual money movement. Financing activities are one of three explanations for why these two numbers diverge.

A second mistake is treating the cash flow statement as a static snapshot rather than a trend document. One quarter of heavy borrowing means little. Three consecutive quarters do. Train yourself to look for direction, not just position.

Frequently Asked Questions

Financing activities show how the organization funds itself — through debt, equity, or returning cash to investors. As a manager, this context shapes every resourcing conversation you have. It explains why budgets expand in some cycles and tighten in others, without anyone explicitly telling you the reason. ---

Financing activities cover transactions that change the company's capital structure — borrowing money, repaying loans, issuing shares, or paying dividends. Operating activities, by contrast, reflect the cash generated or consumed by day-to-day business operations. Knowing the difference prevents a common leadership error: assuming that strong sales automatically mean cash is available for new investments. ---

Review the financing section of the most recent cash flow statement before the meeting and note whether the business is in a capital-raising or debt-repayment phase. Use that context to calibrate your ask — if the organization is actively de-leveraging, frame investment proposals around clear, near-term returns rather than long-term strategic value. It signals financial awareness and increases your credibility in the room. ---

Connect it to decisions they already experience — why a hiring plan was approved or delayed, why a new tool budget was cut mid-year. Explain that the financing section of the cash flow statement shows whether the organization has the structural capacity to fund its plans. Teams who understand this context tend to channel their energy more effectively and waste less time advocating for initiatives that have no realistic financial path. ---

When a business issues new shares, it creates an obligation — not a legal one, but a strategic one — to deliver returns that justify investor confidence. This inflow shows up as a financing activity on the cash flow statement and typically signals a growth phase. In practice, it often means faster timelines, higher performance expectations, and a stronger focus on demonstrable results. As a manager, understanding this helps you align your team's priorities before priorities are handed down to you. ---

Not at all. Financing activities explained at this level requires no accounting background — just the willingness to read a cash flow statement with a management lens. If you can read a basic budget report, you have enough foundation to start drawing meaningful insights from the financing section. The goal is contextual understanding, not technical mastery. ---

Leaders who understand how their organization is financed make better decisions, ask sharper questions in senior forums, and build more realistic plans. Financial literacy — even at this conceptual level — is consistently cited as a differentiator between managers who plateau and those who move into broader leadership roles. It shifts your reputation from someone who executes within a budget to someone who understands why the budget exists in the first place. ---

Once you're comfortable with financing activities, the logical next step is understanding how operating, investing, and financing activities interact to produce net cash flow across a full reporting period. From there, exploring the difference between the direct and indirect method of cash flow reporting will sharpen your ability to spot how non-cash expenses and working capital changes affect what the numbers are actually telling you — skills that translate directly into stronger financial conversations with your CFO or finance business partner.

Types of Receivables explores a complementary area of Accounting, while Understanding Financing Activities focuses on the specific concept covered in this video. Understanding both helps you build a stronger foundation in Accounting.

A basic understanding of Preparing the Investing Activities is helpful before diving into Understanding Financing Activities. If you are starting from scratch, the Preparation of Cash Flow Statement series builds knowledge progressively, so beginning from the first video requires no prior background in Accounting.

The ideas in Understanding Financing Activities show up in everyday Accounting contexts, often alongside concepts like Introduction to Inventory Management. This video connects the theory to practical situations you may encounter in coursework or exams.

After Understanding Financing Activities, the natural next step is Preparing the Financing Activities in the Preparation of Cash Flow Statement series. Following the playlist in order helps concepts build on each other without gaps.

The Understanding Financing Activities video runs for 1 minute, so you can cover the core concept in a single focused study session without needing a long block of time.

Related Micro-courses

11 Concepts

7 Concepts