Loading subject page…

- Accounting

- Recording Financial Transactions

- Understanding Debit and Credit

Micro-course: Recording Financial Transactions

7,374 views

Learn key concepts and earn your certificate.

Understanding Debit and Credit

00:00

01:24

Video Summary: Debit and Credit Explained

Debit and credit basics trip up even experienced managers who suddenly own a budget or must interpret financial reports without an accounting background. Understanding debit and credit — and how every transaction affects your organization's financial position — is a non-negotiable skill when leading teams with cost accountability. Sharper financial literacy means faster, more confident decisions. Watch the full video on JoVE Coach to master this concept with expert-led visuals and step-by-step explanations.

- Recognize how debit and credit entries work together inside the double-entry accounting system to ensure every financial transaction is fully and accurately captured

- Manage budget line items more confidently by understanding whether a transaction increases or decreases an asset, liability, or expense account

- Interpret general ledger reports by distinguishing how each account type responds differently to debit and credit entries

- Structure journal entries correctly so that financial records remain balanced and reflect the true state of team or departmental spending

- Align financial reporting practices with organizational standards by applying the core principle that total debits must always equal total credits

- Build credibility with finance stakeholders by speaking the language of the accounting cycle — from source documents through to trial balance preparation

- Navigate discrepancies in expense reports or budget summaries by tracing entries back to their originating debit or credit recording

- Facilitate cleaner cross-functional collaboration with finance teams by understanding what is debit and credit and how these entries drive reliable financial reporting

Debit and Credit Explained

Picture this: you've just been handed ownership of a departmental budget mid-year. Your finance partner sends over a general ledger extract, and you're expected to review it before a leadership meeting. You see columns of debits and credits, and while the numbers are there, the logic behind them isn't immediately clear. This is one of the most common moments where managers lose confidence in financial conversations — not because they lack intelligence, but because no one ever explained the underlying mechanics in a practical context.

Why Most Managers Struggle With This

The confusion around debits and credits isn't about math — it's about mental framing. Most people encounter these terms through personal banking, where a "credit" to your account means money coming in. In accounting, the same word behaves differently depending on the account type. Assets and expenses increase with a debit. Liabilities, revenue, and equity increase with a credit. That flip in logic is precisely where managers lose the thread. Without a correct mental model, reading a financial report becomes guesswork.

A Framework That Works: The Accounting Equation in Action

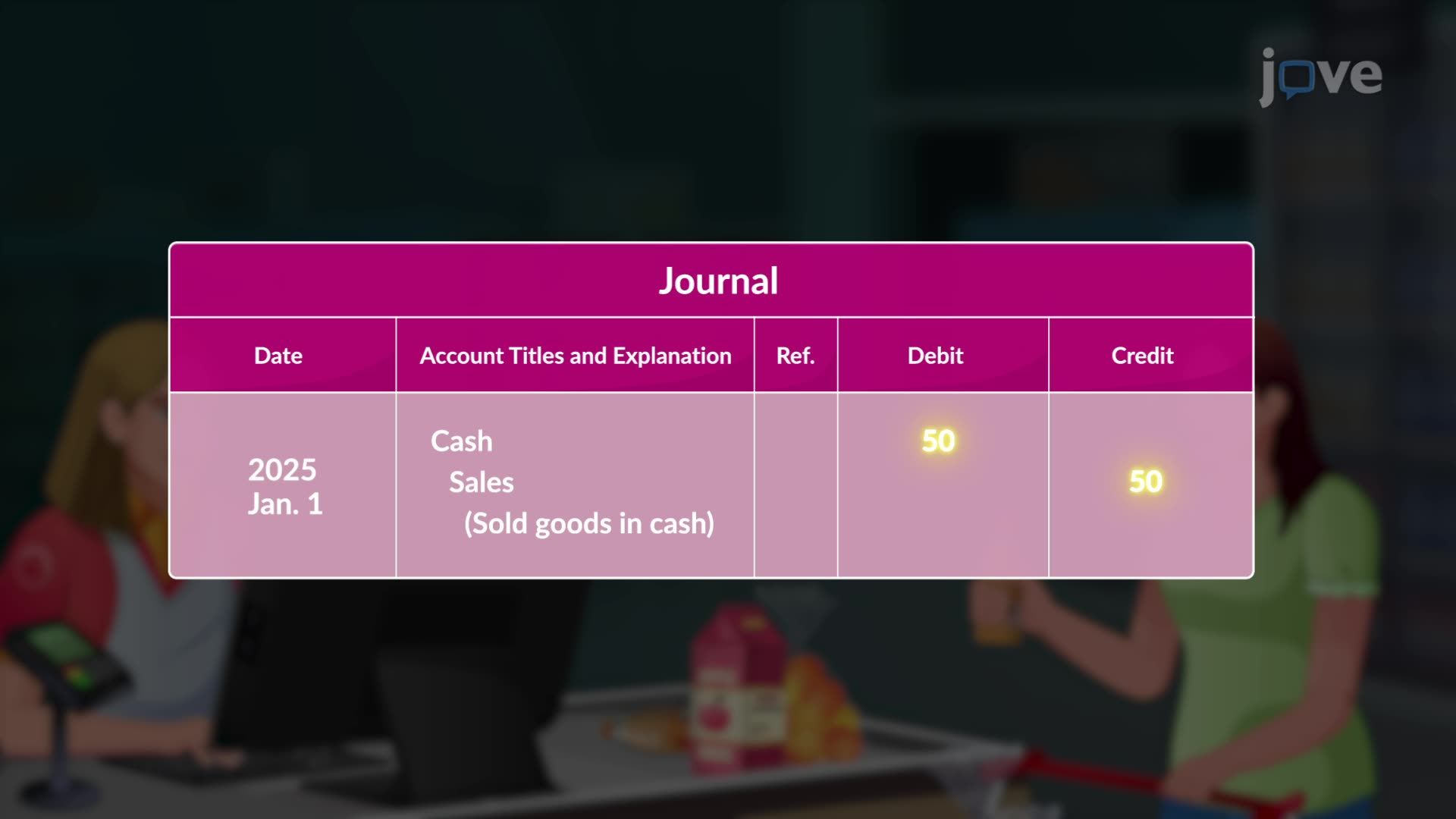

The foundation of double-entry accounting is simple: Assets = Liabilities + Equity. Every transaction you approve — a team purchase, a vendor invoice, a reimbursement — touches at least two accounts simultaneously, always keeping this equation in balance. Think of it as a cause-and-effect structure. When your team buys equipment (an asset increases via debit), the company either spends cash (another asset decreases via credit) or takes on a payable (a liability increases via credit). Neither side of the transaction disappears. This dual recording is what makes the accounting cycle reliable and auditable — from source documents right through to trial balance preparation.

A practical framework to apply here is the T-Account Model: visualize every account as a T-shape with debits on the left and credits on the right. Before approving or reviewing any financial entry, ask: which accounts are affected, and which side do they sit on? This single habit dramatically reduces errors in budget reporting.

How to Apply This in Your Next Finance Review

When reviewing expense reports or budget summaries with your finance team, stop treating the numbers as a black box. Ask your finance partner to walk through one sample journal entry with you — ideally one tied to a recent team expense. Identify the debit account, the credit account, and confirm they balance. This isn't micromanaging finance; it's building the financial literacy to ask better questions and catch anomalies early.

When onboarding a new team member with budget responsibility, share this principle upfront: every financial action has two sides. Train them to think in terms of what goes up and what goes down with each transaction, referencing the account type. Teams that understand this basic accounting logic submit cleaner expense documentation, generate fewer correction cycles, and build stronger working relationships with finance departments.

Common Mistakes to Avoid

The most frequent managerial mistake is assuming a debit is always "bad" and a credit is always "good" — a bias carried over from personal banking. In reality, debiting an expense account is the correct and expected recording for any legitimate business cost. A second common error is treating journal entries as a finance-only concern. In organizations where managers hold budget authority, understanding how their decisions translate into accounting entries is part of responsible leadership. Ignoring this creates gaps in financial oversight and erodes trust with senior stakeholders.

Frequently Asked Questions

For a manager, debit and credit are simply the two-sided recording mechanism that captures every financial decision your team makes. A debit records an increase in assets or expenses; a credit records an increase in liabilities or equity. Understanding this helps you read financial reports accurately, spot errors faster, and have more productive conversations with your finance partners without needing to rely on them to interpret every number. ---

When you understand that every transaction affects at least two accounts and that debits must equal credits, you can quickly identify whether a reported figure makes sense or whether something has been misclassified. Instead of nodding along while finance presents numbers, you can ask targeted questions — for example, why a particular expense account has increased when no team spend was approved. That kind of engaged, informed participation signals financial maturity to senior leadership. ---

Every expense your team submits will eventually be recorded as a debit to an expense account and a credit to either a cash or payable account. When you approve an expense, you're authorizing that double-entry recording. Knowing this means you can verify not just whether the spend was appropriate, but whether it's been coded to the right account — something that directly affects your budget reporting and year-end financial accuracy. ---

A journal is where transactions are first recorded in chronological order — the raw log of financial activity. A ledger organizes those same entries by account type, giving you a running balance for each category. As a manager, the ledger is the document you're most likely to review, but understanding that it originates from individual journal entries helps you trace any discrepancy back to its source — a critical skill when reconciling budget variances or preparing for audits. ---

Start by explaining the dual-entry principle simply: every purchase creates two financial effects simultaneously, and both must be recorded accurately. Walk them through one real example using a recent team expense — show them the debit to the expense account and the credit to the payment account. This practical grounding, rather than abstract policy briefings, builds genuine financial responsibility and reduces the risk of miscoding or documentation errors that fall back on you as the manager. ---

Not at all — debit and credit basics are learnable at any stage of your management career. If you can understand that every financial action has two sides that must balance, you already have the core mental model. The goal isn't to replace your finance team; it's to be a more informed, credible leader who can engage meaningfully with financial data and make better resource decisions for your team. ---

Managers who understand how financial entries work are consistently more trusted by both their teams and senior stakeholders. You become the person who can bridge operational decisions and their financial consequences — a rare and valued capability at mid-management level. Over time, this fluency positions you for roles with greater budget authority, P&L responsibility, and cross-functional influence, because organizations promote leaders who can connect day-to-day decisions to financial outcomes. ---

Once you're comfortable with how individual transactions are recorded, the natural next step is understanding how those entries flow through the full accounting cycle — from source documents and journal entries through to trial balance preparation and financial statement generation. Building this end-to-end view transforms you from someone who can read a ledger line to someone who understands how the entire financial picture of your department is constructed and reported.

Introduction of the Income Statement explores a complementary area of Accounting, while Understanding Debit and Credit focuses on the specific concept covered in this video. Understanding both helps you build a stronger foundation in Accounting.

A basic understanding of Understanding an Account is helpful before diving into Understanding Debit and Credit. If you are starting from scratch, the Recording Financial Transactions series builds knowledge progressively, so beginning from the first video requires no prior background in Accounting.

The ideas in Understanding Debit and Credit show up in everyday Accounting contexts, often alongside concepts like Introduction of the Balance Sheet. This video connects the theory to practical situations you may encounter in coursework or exams.

After Understanding Debit and Credit, the natural next step is The Double-Entry Accounting System in the Recording Financial Transactions series. Following the playlist in order helps concepts build on each other without gaps.

The Understanding Debit and Credit video runs for 1 minute, so you can cover the core concept in a single focused study session without needing a long block of time.

Related Micro-courses

16 Concepts

20 Concepts

17 Concepts